Tax Reform – First Filing Season

October is the time for fall, football and pumpkin-spiced everything. (Here in the south, it’s a time for the heater in the morning and air-conditioner in the afternoon.) What else rounds out the blissfulness of fall? Tax deadlines! October is the extended filing deadline for the 2018 tax season.

The Tax Cuts and Jobs Act passed in late 2017 with many of its provisions taking place in 2018. As a refresher, below is a list of some of the major components relating to real estate business owners and investors. For a complete overview of the tax reform changes, check out my last blog here.

- Expanded Bonus Depreciation – an increase from 50% depreciation to 100% bonus depreciation of certain items with a 15-year life or less

- Qualified Business Income Deduction – 20% of the taxable income generated from a business could be eligible for a deduction pending multiple limitations

- Property Tax Deduction – remained in place for real property trade or businesses

- Interest Expense from Loans – remains deductible for entities generating less than $25 million in gross receipts and are not considered a tax shelter

- 1031 Exchanges – real estate continues to benefit from 1031 exchanges

With our first filing season behind us, we’ve seen firsthand how these reforms resulted in significant tax savings for our investors. In 2018, we completed a $6 million development that yielded over $1.8 million in year one depreciation expense. Prior to the Tax Cut and Jobs Act, only $900,000 of depreciation would have been allowed in year one, with the remaining amount spread across 5, 7 and 15 years.

For individuals, many investors benefitted from the new Form 1040: Line 9 – Qualified Business Income Deduction. This tax revision now offers some tax relief for rental real estate entities rising to the level of a trade or business. The deduction, referenced in bullet point #2 above, provides a 20% deduction from taxable income generated from your qualified trade or business investments. This new deduction has brought about substantial tax savings for individuals, sometimes resulting in the thousands of dollars. This deduction will remain in place through 12/31/2025.

Evidently, real estate investments do provide some tax and asset diversification benefits. When asked about real estate as an investment alternative, Randy Waesche, CFP, of Resource Management, said, “Many of my investors seek real estate as an alternative to stocks and bonds. It adds a level of diversification in asset class, as well as a different risk and return profile. On a risk vs. return basis, investors are seeking real estate for the 6-8% tax-deferred annual distribution that is significantly higher than a short-term municipal bond or ten-year treasury yield. Real estate has many attractive investment qualities. In the low inflation, low growth economic environment we have today, strong tax-deferred returns are attractive for investors. My clients invest tens of millions of dollars in real estate annually.”

As we have previously reported, the Tax Cut and Jobs Act has been beneficial for the real estate industry and we expect it to continue to spur opportunity in the real estate market. At Stirling Properties, we will also continue to find ways to benefit our investors and real estate assets.

Disclaimer: The information contained herein is intended for information purposes only. Individuals should seek advice directly from a qualified professional before making any decisions or taking any action that might affect your personal finances or your business. Stirling Properties is not responsible for any investment or monetary decisions made based on the information provided above and is not a tax advisor. The information provided above was done so with the perceived intent of the legislation and not based on the actual regulations. The actual regulations could yield significantly different results.

Appreciation for Depreciation

The Tax Cuts and Jobs Act contains many major changes to the tax landscape that will affect every type of business entity, both large and small. The new tax reform creates significant opportunities to minimize a business’s overall tax burden.

Perhaps the most impactful—and favorable—legislation to the real estate industry is the changes and modifications to depreciation rules. Here we highlight key components that impact the commercial real estate industry and provide a comparison between the current and new tax laws.

Under prior tax law, most assets held in rental real property were required to be depreciated over periods typically ranging from 5-39 years. Assets with 20-year class lives or less were normally eligible for 50% bonus depreciation, which means we could deduct 50% of the asset in the first year and depreciate the rest over the remaining life of the asset. Under the new law, those same assets are now eligible for a 100% deduction in the year placed in service. Congress has also expanded bonus depreciation to acquisitions, which were not eligible in years past. This is a huge benefit for real estate in many ways, as it allows for significant tax write-offs in the first year for acquisitions, new developments, and redevelopments.

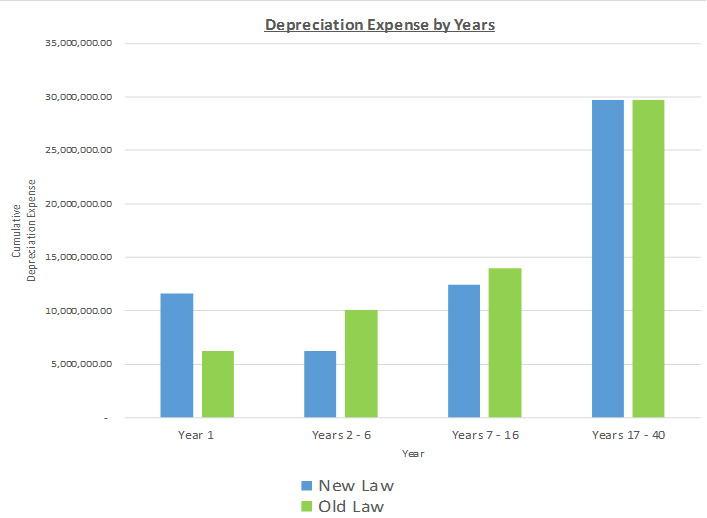

At Stirling Properties, we contract out a cost segregation study on all of our new acquisitions, developments, and redevelopments. These studies allocate the purchase price of the asset into its proper class life. The resulting history allows us to estimate what depreciation will look like on the project during underwriting. On the front end of our due diligence, we have an accurate idea of how much of the purchase price is going to be eligible for the new 100% bonus depreciation. For a $60 million acquisition or development, we estimate that as much as 20% of that investment can be expensed in year one, resulting in over $11 million in depreciation. As you can see in the chart below, depreciation expense has approximately doubled in year one as compared to the old law. The net present value (NPV) of the tax savings resulting from being able to deduct the additional depreciation in year one is over $500,000.

Similarly, ongoing operations of the property will be impacted considerably. To attract and retain high-quality tenants, landlords typically provide tenant improvement allowances which result in enhancements to the occupant’s space that revert to the landlord upon lease expiration. Under the prior law, these tenant improvement allowances were typically eligible for 50% bonus depreciation and the balance depreciated over 15 years. Under the new law, these allowances will be eligible for a 100% deduction in the year placed in service.

Investing in real estate can be a tax advantageous way to deploy capital, especially for individuals or companies that have significant recurring income tax burdens such as financial institutions. We anticipate that the new tax law will lead to higher demand for quality assets helping to keep deal flow robust, thus attracting more buyers and investors into the real estate arena. At Stirling Properties, we will continue to utilize this new tax law for the best interest of our properties and investors.

Disclaimer: The information contained herein is intended for information purposes only. Individuals should seek advice directly from a qualified professional before making any decisions or taking any action that might affect your personal finances or your business. Stirling Properties is not responsible for any investment or monetary decisions made based on the information provided above and is not a tax advisor. The information provided above was done so with the perceived intent of the legislation and not based on the actual regulations. The actual regulations could yield significantly different results.

Tax Reform & Real Estate… It’s a good time for our industry

The Tax Cuts and Jobs Act passed in December and several of these provisions will take effect in 2018. Many individuals have already benefited from the new tax law by seeing their recent paychecks increase. We believe this tax reform will have a similar positive impact on the real estate industry. Tax reform can be a very complicated—and tedious—topic so we’ve highlighted some of the implications for real estate owners, small business owners, and individuals. We’ll preface by saying this is our interpretation of the law, prior to the regulations being written and what we think Congress intended by the text of the law.

Initially, many of us in the real estate industry were very concerned about tax reform and the negative aspects that were being considered. The International Council of Shopping Centers (ICSC), responded by forming a committee consisting of executives and tax professionals across our industry to garner input to deploy lobbying efforts. Stirling Properties played a significant part in providing consistent feedback that guided ICSC’s lobbying efforts. Several executives in our company, including Marty Mayer, Townsend Underhill, Jimmy Maurin, Will Barrois, and me, were active in lobbying congress, and as noted below, these efforts were successful. Together, we were able to quickly respond to aspects of the tax proposal that were detrimental to the real estate industry and offer solutions that would benefit our real estate holdings and the business as a whole. We’ve compiled a brief overview of some of the changes.

Real Estate Business Owners and Investors

- Expanded Bonus Depreciation: Items that were previously required to be capitalized over 15 years (subject to 50% bonus depreciation) are now eligible for a 100% deduction in the year of completion.

- Examples of these items include parking lots, landscaping work, pylon lighting, etc.

- This provision begins to phase out after 5 years.

- Business Income Deduction: 20% of the taxable income generated from a business could be eligible to be deducted from taxable income pending multiple limitations.

- For example, if your share of taxable income from a business you own is $100,000, the first $20,000 may be eligible for a deduction, thus lowering taxable income to $80,000.

- Business income from pass-through entities like partnerships and LLCs will still be taxed at the new lower individual rates.

- Historic Preservation and Rehabilitation Tax Credit: The 20% credit for renovating certified historic structures remains in place but must be taken over a 5-year period as opposed to being fully deductible in the year of completion under the existing law.

- C-Corporations Tax Rate: The corporate tax rate under the new law is 21% as compared to 35% under the existing law.

- Property Tax Deduction: Still in place for real property trade or businesses including rental properties.

- Interest Expense from Loans: Businesses will still be eligible to deduct the interest expense from the debt incurred if its gross receipts are less than $25 million.

- The vast majority of commercial real estate in the Gulf South region would continue to be eligible to deduct interest.

- 1031 Exchanges: Real estate will still qualify to receive 1031 treatment.

- Capital Gains Rates: Remained unchanged at 0%, 15%, and 20% depending on income levels.

- Carried Interest: The new law requires a 3-year holding period to qualify for capital gains treatment as opposed to a 1-year holding period under the current law. This was a “win” for real estate as the original proposal was for carried interest to be taxed at ordinary rates.

Individuals

- Tax Rates: Almost every bracket has been widened and lowered with the top bracket being lowered from 39.6% to 37% thru 2025.

- Standard Deduction: Single filer’s standard deduction increased from $6,350 to $12,000. Married filer’s standard deduction increased from $12,700 to $24,000.

- Personal Exemptions: Taxpayers will no longer be eligible to deduct the $4,100 per dependent.

- Child Tax Credit: The child tax credit increased from $1,000 to $2,000.

- State and Local Taxes: Deduction under the new law is capped at $10,000.

- Estate Tax Exemption: Doubled to $11.2 million for single filers and $22.4 million for married couples.

At the end of the day, the real estate industry appears to have fared well in the Tax Cuts and Jobs Act. Some of these items are pending a technical corrections bill and additional clarification, but the expanded bonus depreciation and business income exclusion make being a real estate investor an enticing proposition. For investors looking to deploy capital in a tax advantageous investment, real estate is an appealing option that will rival alternative investments. We believe tax reform will provide a stimulus for real estate investment over the next five years.

We will follow up with more in-depth coverage of some of these items in the future, as well as how Stirling Properties is adapting to take advantage of this new opportunistic landscape.

The information contained herein is intended for information purposes only. Individuals should seek advice directly from a qualified professional before making any decisions or taking any action that might affect your personal finances or your business. Stirling Properties is not responsible for any investment or monetary decisions made based on the information provided above and is not a tax advisor. The information provided above was done so with the perceived intent of the legislation and not based on the actual regulations. The actual regulations could yield significantly different results.